In the latest edition of the Numbers Report, we will take a look at some of the most interesting figures put out this week in the energy and metals sectors. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers. Let’s take a look.

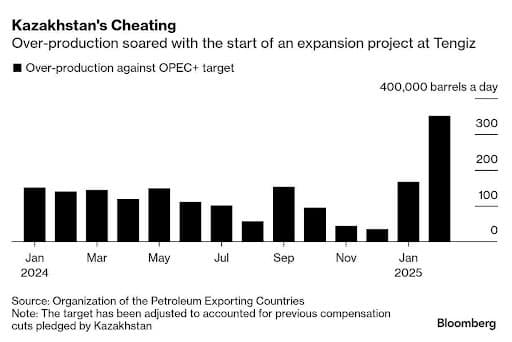

1. Kazakhstan’s Cheating Becomes OPEC+’s Headache

- OPEC+’s decision to speed up its production unwinding in May-July has served the oil group a trick, as collapsing prices only aggravated member countries’ woes about overproducers, most notably Kazakhstan. - The root cause of Kazakhstan’s sudden oil bonanza is the delayed $49 billion Chevron Tengiz Expansion project, officially commissioned in January, that saw production at the Tengiz field skyrocket from 650,000 b/d to 1 million b/d in less than three months. - Kazakhstan’s oil and condensate production reached an all-time high of 2.17 million b/d last month, creating a huge discrepancy between the country’s 1.468 million b/d OPEC+ quota and actual output. - Kazakhstan has fired the previous oil minister last month, with the new minister Erlan Akkenzhenov initiating talks with Western supermajors operating the country’s fields (Chevron, ENI, Shell and others) to cut production by 620,000 b/d.

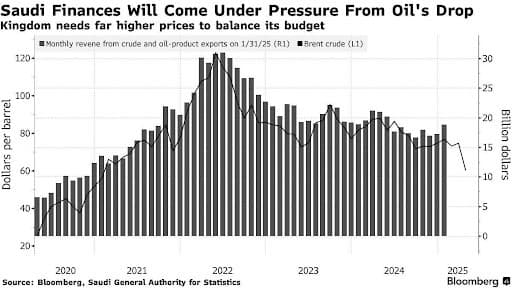

2. Saudi Arabia Reels From Oil Price Collapse, Partly of Its Own Making

- Saudi Arabia has been at the forefront of OPEC+ production unwinding, seeking to benefit from relatively…

Numbers Report – April 11, 2025

In the latest edition of the Numbers Report, we will take a look at some of the most interesting figures put out this week in the energy and metals sectors. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers. Let’s take a look.

1. Kazakhstan’s Cheating Becomes OPEC+’s Headache

- OPEC+’s decision to speed up its production unwinding in May-July has served the oil group a trick, as collapsing prices only aggravated member countries’ woes about overproducers, most notably Kazakhstan. - The root cause of Kazakhstan’s sudden oil bonanza is the delayed $49 billion Chevron Tengiz Expansion project, officially commissioned in January, that saw production at the Tengiz field skyrocket from 650,000 b/d to 1 million b/d in less than three months. - Kazakhstan’s oil and condensate production reached an all-time high of 2.17 million b/d last month, creating a huge discrepancy between the country’s 1.468 million b/d OPEC+ quota and actual output. - Kazakhstan has fired the previous oil minister last month, with the new minister Erlan Akkenzhenov initiating talks with Western supermajors operating the country’s fields (Chevron, ENI, Shell and others) to cut production by 620,000 b/d.

2. Saudi Arabia Reels From Oil Price Collapse, Partly of Its Own Making

- Saudi Arabia has been at the forefront of OPEC+ production unwinding, seeking to benefit from relatively robust demand in the Asian region by adding 411,000 b/d of supply in May, however, the ensuing price collapse is now pressuring Riyadh’s fragile fiscal balance. - According to Goldman Sachs, the budget deficit of Saudi Arabia may soar to $67 billion this year if oil prices continue to trend around $62-63 per barrel, prompting it to cut down on its infrastructure mega-projects and borrow more from the market. - Saudi Arabia’s fiscal breakeven stands around 93 per barrel and it could be as high as $108 per barrel if Riyadh’s mega projects are to be included in that tally, notably higher than Qatar’s $40 per barrel and the UAE’s $55 per barrel. - Saudi Arabia is already the largest bond issuer in global debt markets among developing nations this year, having sold more than $14 billion worth of debt with a potential to raising another $16-17 billion by year-end.

3. Oil Price Collapse Will Force Majors to Cut Buybacks

- As WTI futures traded below $60 per barrel for most of this week, US shale producers have grown visibly more anxious about their future production outlook, as the all-in breakeven has risen above $62 per barrel by now. - The most convenient method of cutting expenses would be to lower (or scrap altogether) share buybacks, with RBC calculating that ExxonMobil’s current breakeven to cover both dividends and buybacks is $88 per barrel, whilst Chevron wields an even higher $95 per barrel. - Upcoming earnings calls of oil majors could shed a light on their respective strategies, overshadowing relatively positive Q1 2025 results as ExxonMobil posted year-over-year profit improvements, to $1.70 per share vs $1.67 per share in Q4 2024. - European majors ENI and BP would find it most difficult to adjust to a lower-price environment as even without share buybacks their breakevens stand above $70 per barrel, in stark contrast to Shell which could relatively easily manage its dividend obligations at $48 per barrel.

4. US-China Trade Wars Wipe Out Clean Energy Investments

- Amidst the US-China trade war, Beijing’s pre-eminent role in wind, solar and hydro technologies has resulted in a continued squeeze on clean energy stocks across the world, with the S&P Clean Energy Transition Index falling 70% from its peak in early 2021. - A number of renewable energy developers have opted for M&A and delist on the back of margin pressures, with Brookfield Asset Management buying France’s Neoen for $6.6 billion and KKR taking over Encavis for $3 billion. - The next wave of M&A is most probably taking place in North America, seeing the likes of Canadian Solar and Fluence plunging by 40-75% in 2025 alone, with a take-private option allowing them to restructure in relative privacy. - Chinese renewable firms are poised to take further market share in Southeast Asia and also at home as Beijing’s total energy transition investment rose 20% year-over-year in 2024, to a whopping $818 billion.

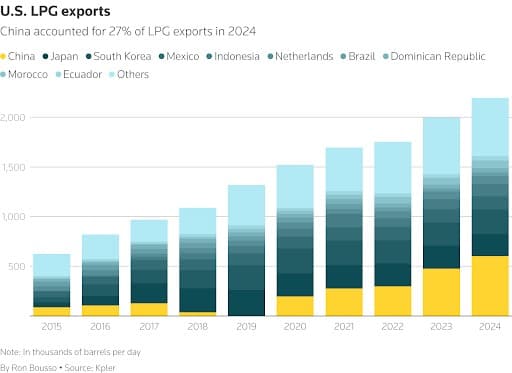

5. LPG Becomes First Casualty of US-China Trade War

- China’s 125% import tariff on US goods will bring to a halt a booming relationship between US LPG exporter and Chinese petrochemical companies, prompting the latter to scramble for alternative suppliers. - The US, being the almost exclusive ethane supplier in the global market, sent a record 5.4 million tonnes to China’s ethane crackers, suggesting that the tariff war would most probably cut ethylene production coming from ethane. - China is also by far the largest buyer of US propane, importing 17 million tonnes last year – more than triple that of the second-largest buyer Japan and equivalent to 33% of all US outflows of propane. - Chinese petrochemical firms are now expected to maximize imports of naphtha, a feedstock that anyways dominates the regional landscape as roughly 70% of ethylene produced comes from it, whilst the most cost-efficient feedstock – ethane – accounts for only 10%.

6. Gas Becomes Germany’s Power Price Trend-Setter

- Germany’s electricity prices are set to be increasingly dependent on natural gas as their link strengthens over the coming years, becoming the marginal source of power generation in a landscape increasingly dominated by intermittent wind and solar. - Germany’s 29 GW coal generation capacity will halve to 14.5 GW by the end of this decade and disappear completely by 2038, coming on the heels of the 2023 decommissioning of the country’s last three nuclear plants. - According to Energy Aspects, natural gas will set German power prices almost 85% of the time by 2028, up some 30 percentage points from the 55% rate expected this year, keeping wholesale power prices in the €90-100 per MWh range. - Europe’s benchmark TTF natural gas futures have been declining since their mid-February peak of €57 per MWh, almost halving to €33 per MWh ($12/mmBtu) by mid-April, however every single remaining month of 2025 is now in contango to the May 2025 contract.

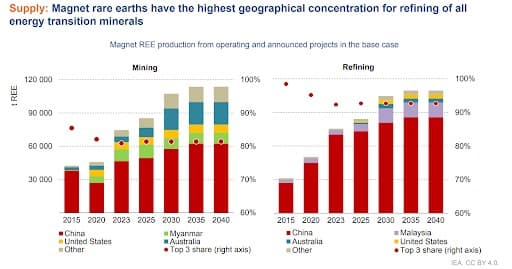

7. Beijing’s Ban of Seven Rare Earths to Take Immediate Effect

- Amidst escalating geopolitical tensions, China’s inclusion of seven rare earth minerals to its dual-use export restriction list will be adding further pain to Western buyers, already roiling from lower inflows of antimony, germanium and gallium. - Beijing controls 90% of global rare earth magnet production, with the magnets themselves also included on China’s export controls list. - If the past example of germanium and gallium is anything to go by, China stopped exporting both rare earth metals to the US months before it announced a full ban in December 2024, suggesting that its current moves are equivalent to a de-facto prohibition to export. - Whilst global rare earth prices are expected to balloon out of control, domestic Chinese prices are decreasing by the day – a kg of yttrium oxide now costs ¥50 ($7/kg), down 10% since the blacklisting announcement.

That’s it for this week’s Numbers Report. Thanks for reading, and we’ll see you next week.

To access this exclusive content...

Select your membership level below

COMMUNITY MEMBERSHIP

(FREE)

Full access to the largest energy community on the web