ASTANA – Kazakhstan is pushing forward a major rollout of digital payment reforms, including an open banking initiative. In an interview with The Astana Times YouTube channel, Binur Zhalenov, a chief digital officer at the National Bank of Kazakhstan (NBK), unpacks what stands behind open banking and the role of artificial intelligence in the country’s financial ecosystem.

Binur Zhalenov is a Bolashak scholarship graduate. He also chairs the National Payments Corporation. Photo credit: The Astana Times

Open banking entails a standardized exchange of financial information between various financial institutions and third-party providers with the consent of the customer. The exchange is provided by Open API (application programming interfaces) for secure access to consumer data.

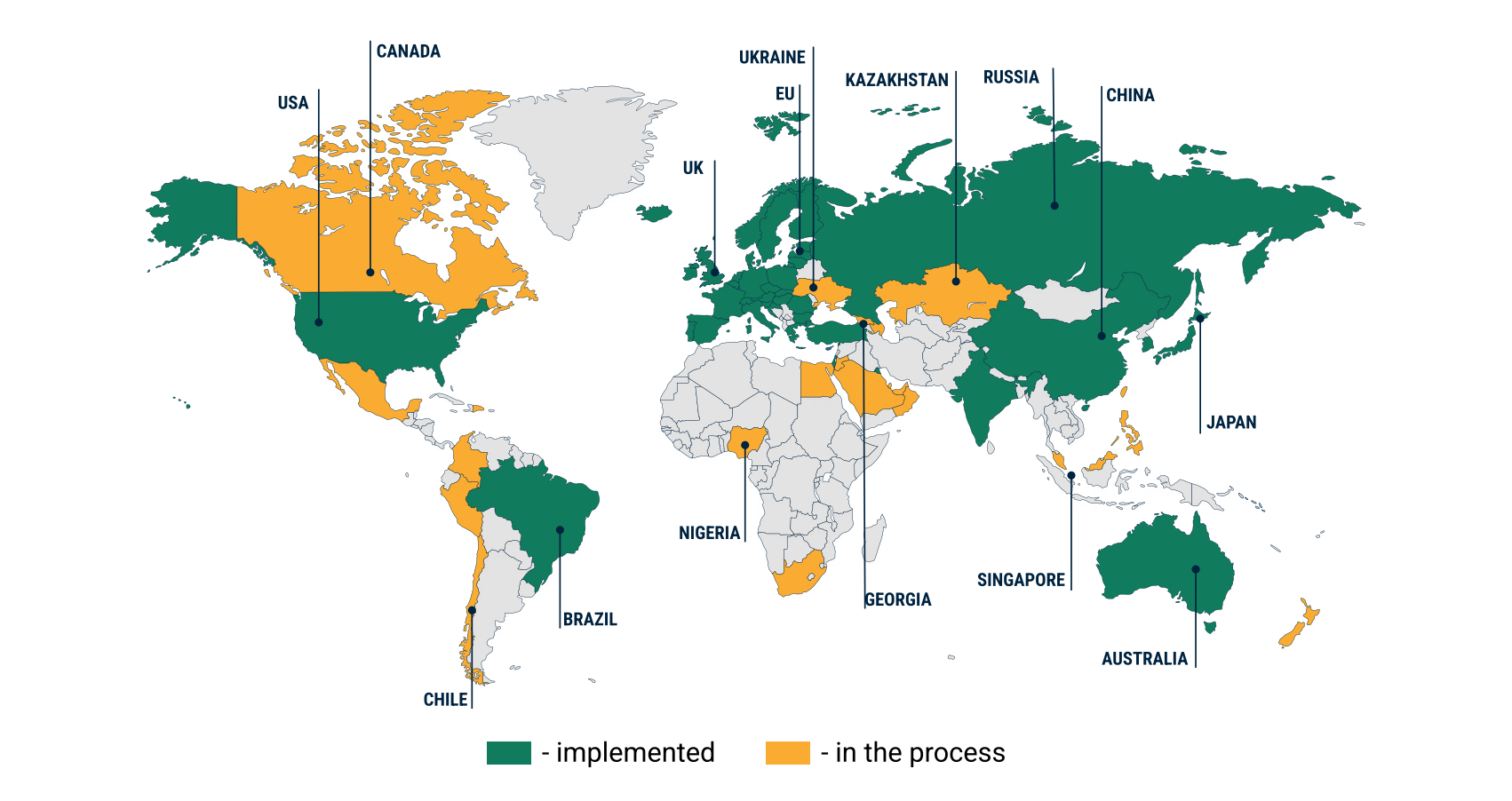

Globally, around 100 countries are exploring open banking at different stages.

National digital infrastructure

In Kazakhstan, open banking is part of the digital strategy that NBK endorsed in 2024 to build what it calls a Digital National Bank. With five key pillars, it is designed to create a comprehensive ecosystem around its central banking and supervisory functions.

The first pillar focuses on establishing a national digital financial infrastructure. The second involves implementing supervisory technology, using artificial intelligence and machine learning, to strengthen oversight of financial institutions.

“The third is a data-driven central bank when we build a so-called data factory that unifies the entire technology stack – from data collection to data analysis – so that all of the decisions in the central bank are made based on data, and we are really focused on that at the moment,” said Zhalenov, who presented the concept of the national digital financial infrastructure to the government last week.

Internal digital transformation and the adoption of agile working practices are the fourth and fifth pillars.

“Open banking is a part of the first pillar,” said Zhalenov. Digital tenge is also part of that effort.

“The idea of national digital financial infrastructure is very simple. As you mentioned before in your questions, Kazakhstan has a pretty mature fintech market. We have a very high penetration of cashless payments, around 86%. They are not just cashless, they are digital. Eight out of ten transactions are made using mobile banking applications,” Zhalenov said.

According to him, this progress stems from a combination of progressive regulation and interbank infrastructure that allows seamless transfers between banks.

“These two factors enable competition. When we have competition in the market, the market participants are forced actually to make innovation to make their consumers happy because they fight for their consumers. The idea of national digital financial infrastructure is to support this competition,” he explained.

To put it differently, Zhalenov described the national digital financial infrastructure as “roads between banks,” allowing money to move freely via “payment rails,” including card payments, peer-to-peer transfers, and QR codes. As a central bank, NBK is in charge of building infrastructure for each of these types.

Consumer dictates

The end goal, according to Zhalenov, is to give consumers more control. Transferring money between banks is often an expensive and cumbersome process, which the NBK aims to solve as part of its broader push toward open banking and a more competitive financial ecosystem.

“We want to build a market where the consumer dictates what to do to the banks, not vice versa. Because, at the moment, there are several banking ecosystems in Kazakhstan, and most of the consumers are locked in this ecosystem,” Zhalenov said.

“It is very hard to send your money from one bank to another because the tariffs are high. When we tackle this issue, the money would move easier, faster, and cheaper, which means that every participant in the market would be motivated to offer something new to keep customers in the ecosystem,” he said.

Open banking explained

The approach that Zhalenov’s team is undertaking has three components. First is interbank payments.

“Last year, we launched a faster payment system when you, with your mobile number, can send money to another bank with a very cheap fee. This year, we are going to connect all of the banks and make participation in the system mandatory. There is going to be a legal mandate for every bank to participate,” he explained.

Globally, around 100 countries around the world are exploring open banking. Photo credit: NBK

The second component is QR payments, a solution that found strong resonance and support among Kazakhstan’s citizens but has so far been limited by bank-specific terminals. That will change, Zhalenov noted.

“What we are going to do is that you have your mobile banking application, for example, Freedom [a second-tier bank in Kazakhstan], and with this banking application, you can pay in Kaspi terminal, for example, or Halyk terminal,” he explained.

The next component is account aggregation.

“What we are going to do is that in your mobile banking application, you provide consent that you are ready to share your data from other banks. When you provide this consent in this banking application, you can see the accounts from other banks,” said the official, highlighting that it would take more time to introduce it due to personal data protection issues.

“Now the consumer will dictate. It will be very easy to switch from one ecosystem to another, which will drive more competition in the market and which automatically will make the fees lower and innovation some more intense,” he said.

In 2025, Kazakhstan is set to advance its open banking framework with broader functionality and more integrated digital interactions, including shifting toward product-oriented Open APIs, enabling a wider range of sophisticated financial products and services.

The full launch of peer-to-peer mobile number transfers is scheduled for the first half of this year. The QR payments are going to be introduced also this year.

What about data privacy, then?

As Kazakhstan pushes for digital transformation, concerns about data privacy remain top of mind – both for regulators and the public. To address this issue, Zhalenov said NBK relies on two tools – stricter regulation and enhanced technology.

“Every year, regulation becomes stricter and stricter. For example, we have, as a benchmark, GDPR [The General Data Protection Regulation] in the European Union, which has a very strict regulation. In Kazakhstan, the regulation is much more liberal,” Zhalenov said.

A new banking law is now in the making following President Kassym-Jomart Tokayev’s directive. It will have a dedicated chapter on data privacy and protection.

Countering fraud

Concerns, however, are not limited only to data. Fraud, particularly digital fraud, has also become a pressing issue for the country’s financial sector.

In 2024, working with banks and law enforcement agencies, NBK launched the Anti-Fraud Center, which is designed to help financial organizations spot and stop fraudulent transactions, react quickly to suspicious activity, and share information instantly with each other. The center also keeps a single database of all fraud-related cases.

Assel Satubaldina and Binur Zhalenov during the interview. Photo credit: The Astana Times

Based on an information-sharing scheme, this center creates a shared fraud-alert system that links the anti-fraud infrastructure of individual banks into one network.

“If an incident happens, let’s say in Halyk Bank, automatically everyone knows about that, knows the fraudster, the requisites, and we block these fraudsters in every bank. It helps us to prevent money leakage,” he explained.

Zhalenov revealed that the center blocked 1.5 billion fraudulent transactions with nearly 300 million tenge ($579,820) giving back to people who suffered from the fraud.

Does AI have a role to play?

AI is rapidly becoming applicable to almost all sectors, and fintech is no exception. Zhalenov said NBK is exploring 55 use cases of AI – from a chatbot trained and educated on NBK data to more advanced tools that assist with capital flow monitoring, compliance, and fraud prevention.

“We are going to use AI in financial supervision. For example, our partners, the financial agency [Agency for Regulation and Development of Financial Market], they are now implementing SupTech solutions that help them to accelerate different business processes related to financial supervision,” Zhalenov said.

With nearly 1200 market participants subject to supervision, it entails a huge amount of data. With AI, this process can be streamlined.

“The huge amount of data and AI helps us to process it much better and easier; most importantly, to identify potential risks at a very early stage. Not just when it occurs, but to predict,” he explained.

The central bank is also eyeing AI to support its investment operations. As the manager of Kazakhstan’s National Fund and Unified Accumulative Pension Fund, it sees strong potential in using AI to enhance investment decision-making processes.

When asked about AI’s overall impact on the country’s fintech market, Zhalenov said it is going to be huge. Based on the survey the team conducted last year, more than a third of market participants use AI in their services, and Zhalenov expects this number to double.

Most financial institutions currently deploy AI for front-facing functions, such as customer engagement and communications. Expectations are high that the application will shift to more complex uses.

More personalized financial services

Zhalenov noted the advancement of technologies is likely to make financial services more personalized and have a greater customized user experience.

“At the moment, for example, a bank offers you a generic offer of credit. You apply and wait. I believe in the future, for every particular consumer, they would have already a dedicated offer,” he said.

Does that mean that customers will be more tempted to buy things? Probably. But it also reflects a shift in how financial institutions interact with customers — moving away from a one-size-fits-all model to a data-driven, behavior-informed approach.

Stay tuned for a full interview with Binur Zhalenov coming this week on The Astana Times YouTube channel.